What Not to Say to a Car Salesman [List]

Ever wonder what not to say to a car salesman? Or how to deal with car salesman? We’ll teach you what not to say.

They are not all the same but if you’ve shopped the internet long enough you’ve come across a dealership that isn’t honoring internet price listed on either their own website or another ad site like cars.com.

Ever hear of it?

Yeah, me too.

Even as a professional car buying concierge and a professional negotiator, I’m not sure why, but I still ask the question “So, are you saying that you are not honoring the internet price?”

The question remains. Does a car dealership have to honor an online price especially when it’s a dealer ad?

Most of the time, there is specific small print language within their ads that explains what is missing from the online price. And there is definitely small print on their website explaining the price.

The dealership website states that the price includes all applicable rebates; we cannot qualify for all of the rebates.

I’ve actually never seen it happen where someone qualifies for every rebate offered. They are never easily combined. So, even calling it a lowest “possible” price seems unrealistic. It’s actually not possible.

There are also some other requirements you must meet including selling a trade-in.

And of course, most consumers should know by now that tax, title and registration are not included in the online price.

What are administration fees? They are hard to define. Those fees are often referred to as doc fees or documentation fees. Regardless of what it is called (they vary from dealership to dealership), it’s simply a profit center for the dealership.

I see this all the time.

Just like you, I use car search sites like Car Gurus, Auto Trader, Cars.com and search for the vehicles.

I enter the make, model, trim, color, miles and any other feature needed.

Then the trouble comes. You sort it by price.

Herein lies the problem.

The dealerships will set the price they want to SHOW you. This is not necessarily the price they are willing to sell the vehicle for.

They simply understand the way consumers are searching and/or sorting. By PRICE.

The price they SHOW you is not the entire picture.

Then, the car research website may even state the vehicle you’ve found (at the top of the list) is a great deal.

Right?

Well… maybe, or maybe not.

Chances are, the great deal advertised (much lower than everyone else) may not be giving you the entire picture.

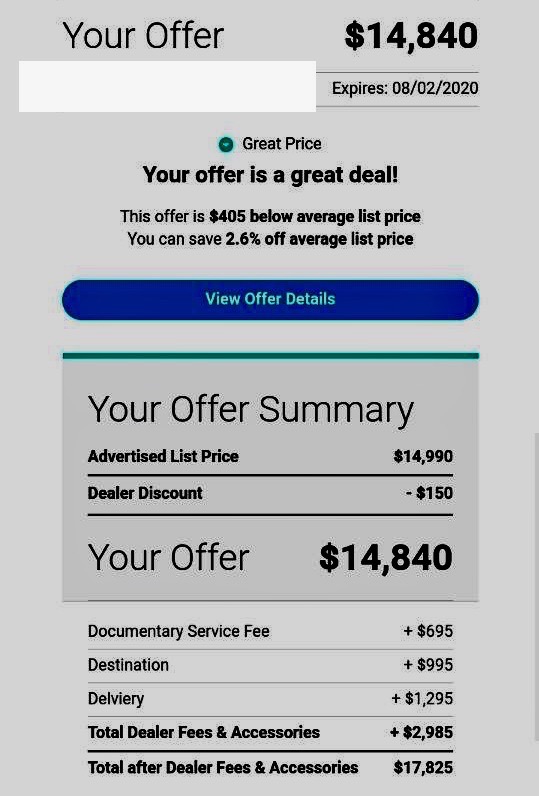

Now look at this online offer.

This quote, from a large online lead generation tool for dealerships (and your car research site), shows that this is a great deal.

The offer is $405 dollars below the average list price.

The keyword in that sentence is list price.

What is the $2,985 in dealer fees and accessories?

That eats up the $405 dollars quick, right?

It also wasn’t quite easy for me to find the breakdown of these additional fees.

You have to know where to look to find it.

You have to actually reach out to the dealership in a lot of cases. Some dealerships do not disclose these fees anywhere online. If they do, they are rarely out in the open. Therefore, you’ll need to scroll down, open another window or find the smaller print.

The average consumer only sees the price of $14,840 for the car and thinks it is a great deal.

They spend their time visiting the dealership and fall in love with the car. When the numbers are presented, the focus is set on the payment not revealing the actual cost of the car.

Consumers who spend hours at the dealership, accept the fact of the car dealer not honoring internet price. They accept it because they don’t want to go through the whole ordeal again somewhere else.

The dealer charged more than the advertised price. Simple as that.

A car dealer not honoring internet price should, in this day and age, be nothing new. In fact, the point of this post is to inform you what to look for when you’re doing your car research online.

The dealerships use the internet for one thing, to find a way to get you into the dealership.

You’re doing your research, so be aware, it’s highly unlikely a dealership will honor that internet price you see. Assume some added costs especially tax, title, tags. You also need to call them to get a real breakdown of the deal, any dealer add on’s and preferably get it in writing before you even visit.

I rarely recommend negotiating at the dealership.

Good luck out there. Tell us in the comments if you find a dealership that honors the actual online price, we’d love to know so we can work with them!

If you need help, schedule a free strategy call with an expert.

Watch this short video to find out why working with Your Car Buying Advocate makes all the sense in the world.

“Internet pricing” for cars at dealerships refers to the pricing strategy that dealerships use when advertising and selling vehicles online. There are a lot of issues with internet pricing on free car buying sites because the prices set are typically not the price that dealerships deliver on when you go to their dealership.

Taxes, title, documentation fees and any dealer markups, addendums they choose to add are not included in internet prices.

The purpose of listing a lower internet price for dealerships is to attract consumers to their dealership. If they can get you to the dealership spending your time there at length, it is highly unlikely you will want to go anywhere else and spend more time doing the same. It’s just a marketing ploy. When a dealership lists a price lower than everyone else, they are aiming to show up first in the list of vehicles sorted by low price. They get more eyeballs, and likely more customers that way.

You need to call the dealership who is listing the vehicle and ask for a breakdown of the pricing of the vehicle. You can ask for a buyer’s order or a menu as it’s called by some dealerships.

Some listings or advertisements may claim a particular payment or price and it could be only for particular buyers or incentives for those with specific qualifications. Reading fine print will help but talking specifically to the dealer is necessary to get the actual pricing details.

Every dealership no matter the make or model has fees.

To know the total cost of a vehicle, you must get a buyer’s order from the dealership. There is no percentage or estimated amount that one can guess or say based on a posted internet price.

Ask for a buyer’s order which should detail out the total price of the vehicle. Ask for the out the door number with tax, title and fees included. You can ask for this information over the phone, there is no reason you need to visit the dealership to get the total price of a vehicle. But be prepared for dealerships to try to get you to come in to give you that information.

Rebates and incentives are often advertised to everyone but the fine print will often disclose who or in what situation the incentive or rebate can be applied to. Additionally, you can’t usually combine incentives or rebates. It’s usually a one or another offer but advertisements won’t typically disclose that up front to get you in the door.

Doc fees or documentation fees are simply profit centers for dealerships and each dealership can have a different fee. Some states have max doc fees set.

If you want the best price or deal you need to make dealers compete. It would take a lot of time if you visited 4-5 dealerships to get pricing on a vehicle. That’s why we recommend that you locate 4-5 dealers with the vehicle you want to purchase and contact each of them to get a buyer’s order. Once you do that, you can see the difference in price between each dealer. You can then begin to negotiate so that you know what to expect to pay and can do your due diligence. If you don’t contact more than one dealership and simply walk on the lot, you cannot know if you’re getting the “best” deal you can get because you haven’t made dealerships compete.

Once a dealership gets you in the door, you are less likely to go anywhere else. Dealers’ best tactics are to get you to spend time sitting in the vehicle, test driving, sitting at the sales desks, where you waste and invest a lot of your time and day. This breaks a lot of consumers down so they overlook a lot of sales tactics like a lower online price that turns out to be much higher. Often dealers will list low prices or mystery vehicles that don’t even exist on the lot. When you get there you find out that the vehicle is “sold” or no longer there.

Call them and ask them to send you a buyer’s order by email or even text message. Transparent and upfront dealers will send it to you without a problem. Those who refuse to send that information want you to come into the dealership. That’s a bit of a red flag.

Simply walk away and find a dealer that will be upfront and transparent with their pricing. You can also leave a review so others know what to expect.

Ever wonder what not to say to a car salesman? Or how to deal with car salesman? We’ll teach you what not to say.

Derek Suarez serves as a YCBA car concierge in Raleigh, North Carolina. He also works with and for car buyers spread all over the USA.

To make car dealers compete for your business, you’ve got to put in a lot of work. Dentist of dealership? If you ask 100 people

Get car buying resources & secrets from Mike, former car salesman and join our growing community. Opt out any time, we never spam.

Want kept in the loop?

We don’t spam you and we never share your info with anyone.

Want our help to save time and sanity while doing the car buying thing? Schedule a free strategy call.

This Post Has 7 Comments

Hi Mike,

What about when the 0% or 0.9% comes directly from the manufacturer? I have been shopping for a car and have walked out of dealerships twice because after we have agreed on a price they then try to raise the price after I insist on Manufacturer’s financing, which I qualify for because I have Tier 1 credit. They have claimed that I can’t take both the “rebate” or the 0% but in both cases there has been NO rebate advertised on the manufacturer’s website, neither on the dealer’s web site, neither the manufacturer says “0% offer cannot be combined with other incentives”. Neither the price quote breakdown said “this price includes a rebate, incentive etc”. Despite nothing saying anything about being either/or, one of the dealers insisted that I could only pay the quoted price if I use “conventional finance” vs the Toyota 0% 48 months APR. It feels that I am being penalized for having good credit. The most annoying thing is that in one case my husband test drove the car and got a quote. Told the salesman he had to talk to me before making a decision and came back home. Hours later the salesman called to follow up and he told him that I was NOT interested in buying unless I had Toyota financing at 0%. The salesmen said that would be ok and we agreed to meet later to finalize the purchase. As soon as we arrived, I discussed financing with the salesman. Then he went on about how they are not really making money on the deal if I do 0% (after he said on the phone that it was ok). After much talk, I finally agreed to 60 months 0.9%. We signed some papers, reviewed the quote, the credit application, etc. Then about 2 hours into the paperwork, the salesman comes out with the finance manager who tells us that he could not give me the price on the quote unless I used “conventional finance”. Or that I could do 0% or any of the other low APR offers from Toyota but he will have to raise the price of the car by $2,250. Why did he not say that on the phone? Or as soon as I arrived? At that point, I was upset. I had been at the dealership almost 2 hours and it was NO surprise to them that I only wanted to finance from the manufacturer. It was not something I kept a secret, I told them before I even left my house. So to pull this 2 hours into the deal just felt wrong. He suggested that I pay off in full to get the low price, (which my husband and had previously considered since we were putting 50% down). I just I did not feel like it, not after they made me waste 2 hours. If they had been completely honest about what the price included before I left my house I would have understood, but pretending to be ok with 0% finance at 48 months, then convince me to do 0.9% at 60 months after I stepped on the dealership (which I agreed to) then make sign a price quote knowing that I wanted only Toyota financing and then try to change the deal at the eleventh hour it was too much. So of course, I said thank you very much, I completely understand your dilemma you can keep your car. At this point, I don’t understand why Honda, Volkswagen, Hyundai offer these “low APR” offers if the dealers are not willing to honor them. In both occasions the finance managers appear to be upset at me because I’m planning on doing manufacturer’s financing. Buyers with Tier 1 credit are being penalized for using manufacturer’s financing. I understand that some manufacturers offer EITHER a cash incentive OR low APR offers, but in both of these cases the manufacturers did NOT have any advertised incentive or rebate that I was getting “in lieu of” the 0% financing. Why should I pay a higher price for a car only because I have good credit? And if I am writing a $25,000 personal check to pay a dealer right then and there, then I feel that I deserve an even bigger discount. It feels that dealers want unreliable buyers with bad credit. What ever happened to “cash is king”? At this point, I feel that I should be walking in at the dealership saying, I am a “cash buyer”, what is the lowest price I can get on this? Any suggestions?

Ted,

Thanks for the comment.

Buying a vehicle is a very complicated transaction. This situation comes up quite frequently. Even if the manufacturer doesn’t list rebates it doesn’t mean they do not have incentives they give to dealerships to help them sell vehicles. The dealership gets to choose whether or not they give those incentives to you or if they keep them. The bottom line is you can not make the dealership sell the vehicle for any less than they are willing to sell it for. The real question now is which dealership has given you the best deal. I would buy that one as you are probably getting pretty close to the bottom.

My advice in your situation would be to not take the special financing. Especially if you have a substantial down payment or could pay cash.

My credit got ran for a pre approval and buy online through a car dealership. The dealership messed up on price but my financing was approved and credit was ran. All I had to do was go in and sign papers. Is the dealership under any obligation to honor the price since my credit was ran.

This is great information! Thank you for sharing this. I know I’m on the right track. I asked some of the very same questions without knowing this. Initially, a quick google search of the phrase “internet pricing” led me here! thanks again!

Thanks Niki! Be sure to subscribe to our youtube page to get more content!

CJ Hi Mike what if a dealer list a car on inter net car max at a set price you want to pay cash for it at that price he states to get it at that price

you have to finance it through them at the msrp price which is a lot higher.

Hi CJ, typically the price listed on these sights by dealers and even on their own sites will rarely ever be the out the door price no matter what. And a lot of them have disclosures in fine print that will say you need to qualify with x,y,z to get that price or that tax, title is not included. Whether they want to honor the price they list for is totally up to them. I find it to be an unethical practice not honoring what they document online, but that’s how a lot of them operate. It’s up to you, who you choose to do business with.